Campground Software Primer - The Software Pulse

Market Maps, Major Trends, and White Spaces

“The campground industry is kind of like the ag industry: It always seems like it’s 10 years behind. If you look at campground websites, a lot of times, they look straight out of 2004. These are hardworking people, and they don’t have time to work on their websites.”

0. Intro

Switching up the content – today we’d like to introduce our first deep dive into what we believe is a heavily undercovered vertical market for software: Campground/RV Park Software.

The US campground and RV park industry is characterized by low concentration and innovation, producing roughly ~$10.9B in revenue in 2025.

There are around 16,500 businesses in the industry, with 78% of those being mom and pop shops. The Annual 2023 Outdoor Hospitality benchmarking report doesn’t even mention the word “software” once in the entire report, leading us to believe that most non-consolidated operators are still using pen-and-paper or legacy systems.

Looking at the 2025 KOA report, only 55% of campers report using mobile apps to book campgrounds, find activities, and access weather updates. Additionally, a majority of discovery is still coming from horizontal funnels such as social media (68%) and online reviews (74%). This low consumer adoption gives us more confidence in our thesis, suggesting there still is no dominant camping-native software platform for management and discovery.

We believe this fragmented, under-digitized end market, combined with consolidation pressure from REITs and private equity, has enabled a unique opportunity for software to be used as a lever for margin expansion and drive growth via discovery. Campground software has a simple value proposition: basic digitization of reservations, payments, and operations for an industry that’s lagging a decade behind.

1. Overview

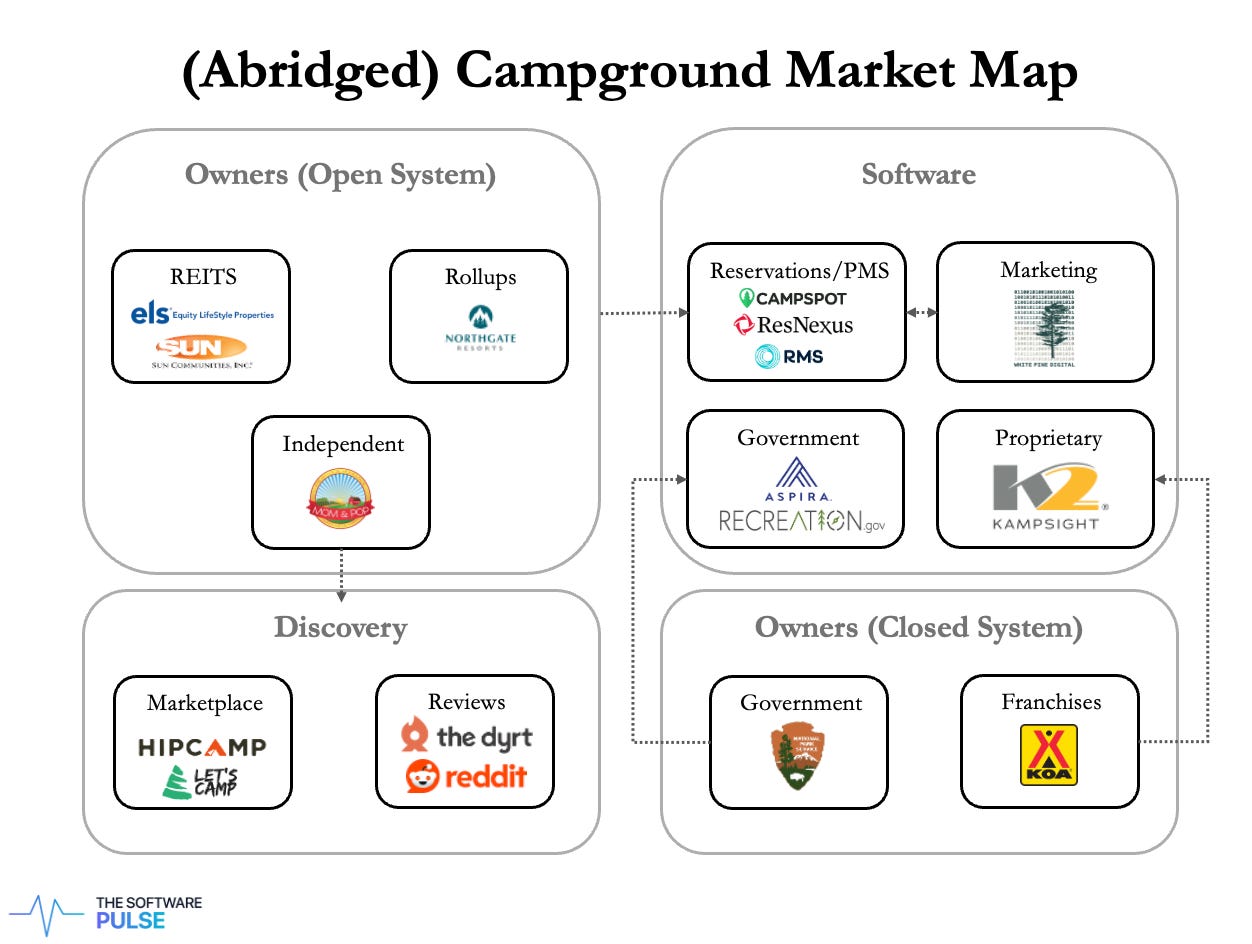

1.1 Market Structure

Supply

On the supply side, there are five primary ownership categories in the campground market, each with distinct software needs and procurement cycles. Of those five ownership categories, 3 of them can be considered consolidators (REITs, Rollups, and Franchise Systems)

REITs: Enterprise buyers with sophisticated procurement and multi-property management needs.

Equity LifeStyle Properties (NYSE: ELS) operates over 450 properties across 35 states with more than 172,850 sites, and 226 RV resorts/campgrounds (91,000 sites).

PE Rollups: Growing fast through acquisition, creating demand for scalable software.

Northgate Holdings demonstrates vertical integration: acquire/develop luxury camping resorts, build software (Campspot) to manage operations, offer software to third-party campgrounds, then create an ecosystem of ancillary services (White Pine Digital for websites).

This seems to be one of the most interesting models from a software perspective, with the property operator becoming the software vendor similar to Growth Buyouts

Franchise Systems: Closed ecosystem with software bundled into franchise fees, rather than charged separately

KOA operates 520+ locations with proprietary tech (K2 platform)

KOA’s approach bundles software as a franchise benefit, creating a closed

Campgrounds converting to KOA see 19% first-year revenue increase on average

Government Agencies: National/state parks. Long procurement cycles, specialized requirements.

Government and state parks have largely resolved into (mostly) efficient markets. The two winners that emerged were Aspira, and Recreation.gov (a Booz Allen contract).

Aspira (ReserveAmerica)

Ownership: Alpine Investors (acquired from Vista Equity Partners in April 2021)

The dominant player in government outdoor recreation software with a 30+ year track record:

Independent Owners: Mom-and-pop operations dictated by price-sensitive, relationship-driven sales.

We believe this is the layer where most software vendors should compete, and where the most competition is. Two models dominate:

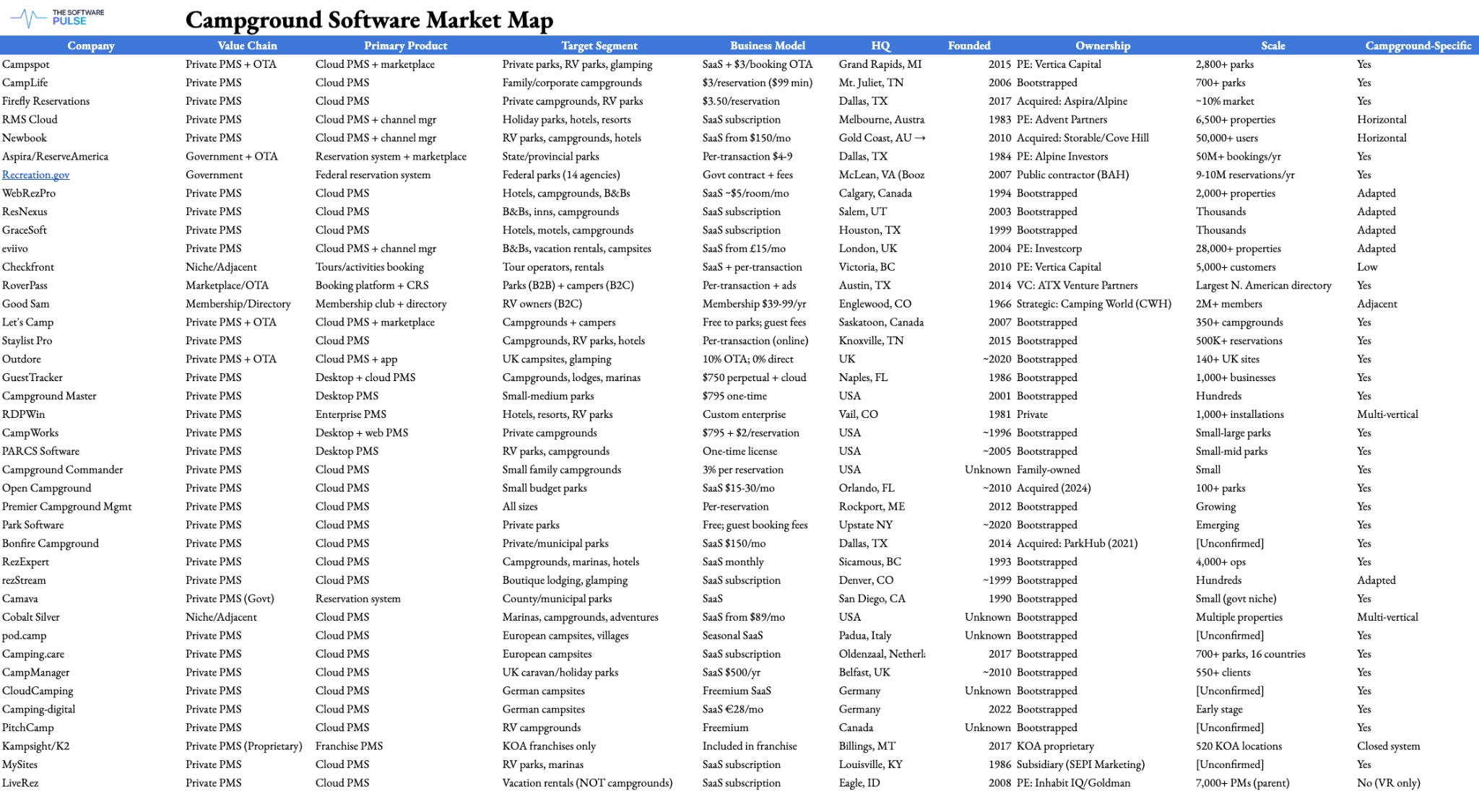

Campspot (The emerging category leader)

Founded: 2015 in Grand Rapids, MI

Ownership: Backed by Vertica Capital Partners (Feb 2025)

Business Model: $3/booking + marketplace commission (~10%)

Campspot is trying to build a dual model (attacking PMS and marketplace), and create a flywheel: more parks on the platform → more inventory for campers → more bookings → more value to parks.

Marketplace still hasn’t fully found PMF yet; only drove 4% of bookings in 2023

We suspect OTAs are still driving a majority of bookings

ResNexus (The flat-rate alternative)

Founded: 2003 in Salem, UT

Business Model: Flat monthly fee starting at $30/mo (no transaction fees)

Appeals to price-conscious operators who want predictable costs

High-volume parks may prefer flat fees, while low-volume parks benefit from usage-based pricing.

Demand

On the demand side, campers mostly book through consumer OTAs (Hipcamp, The Dyrt, Campspot Marketplace) taking 15-20% commission, government platforms, membership networks like Good Sam, or directly via property websites and phone.

Consumers mostly book through OTAs and online marketplaces. Campspot has been trying to vertically expand into this space, but it seems like early winners have emerged and won consumer mindshare. Only time will tell whether these businesses have true moats, or simply just brand recognition.

Hipcamp (“AirBNB for Camping”)

Founded: 2013 in San Francisco, CA

Ownership: Index Ventures, Andreessen Horowitz, Benchmark, Bond Capital

Business Model: 15-20% commission

Acquired Youcamp (Australia, 2020), Cool Camping (UK, 2022), BookOutdoors (Oct 2024)

Unlike PMS vendors, Hipcamp focuses on unlocking private land (farms, ranches, vineyards) for camping, expanding total supply rather than digitizing existing campgrounds.Demand

1.2 Software Stack

Campground software can be broken into four functional layers. Campgrounds are still consolidating functionality into all-in-one platforms:

Reservation/PMS: This is the foundational layer of campground operations. PMS (property management software) handles booking calendars, check-in/check-out workflows, guest profiles, and payment processing. This is arguably the most mature part of the industry, although new cloud-native players have emerged (e.g. Campspot) who have been displacing legacy desktop software. We suspect continued M&A in the reservation/PMS space as more private capital flows into the vertical, and market leaders start acquiring some of the smaller more fragmented players to win market share.

Channel Management: This layer is less prevalent in standalone software. Channel Management connects campground inventory to third-party distribution channels (OTAs like Booking.com, Airbnb, and Hipcamp, and membership networks like Good Sam). Typically for hotels, these features were standalone as they emerged like Siteminder/Cloudbeds), but channel management for campgrounds has largely been absorbed and bundled into PMS platforms, with some exceptions.

Revenue Management: This is the clearest white space for campground software. While hotels adopted dynamic pricing decades ago, campgrounds still price seasonally with manual adjustments. We believe that the winner in vertical software will be whoever develops the best solution here. In 2023 Campspot processed $1.9b in bookings, but only saw $5.3M in revenue from dynamic pricing features. KOA’s K2 platform offers yield optimization, but is locked behind the franchise system. Hotels saw 5-15% revenue lift from sophisticated revenue management; if software offered similar gains for campgrounds, owners would scramble to sign up and expand their margins. This seems to be the clearest product expansion pay for leaders, or a greenfield entry opportunity for a specialized vendor to win.

Website/Marketing: This part of the stack is the least specialized, encompassing website builders, SEO tools, email marketing, and reputation management. Direct bookings are the highest-margin channel (since OTAs charge commission), so software that drives guests to book directly has a clear ROI. The leaders that have broken out here are White Pine Digital (part of the Northgate/Campspot ecosystem), and ResNexus who offers integrated website solutions. However, the layer still remains fragmented with many parks using generic website builders like Squarespace/Wix, or local agencies. A vertically-integrated marketing suite that combines website, SEO, email, and review management (like Lodgify or Guesty for rentals) has yet to win.

2. Major Trends

We’d like to highlight 3 major trends surrounding this ecosystem.

Firstly, camping went mainstream. The pandemic accelerated adoption dramatically; 58 million households camped between 2020-2023, and 11 million more households camped in 2024 vs. 2019. This adoption change also came with a significant demographic shift. GenZ nearly tripled in market share, going from 9% in 2019 to 22% in 2024. We believe this will be a significant tailwind for software, as younger campers flock to digital-first booking experiences, not phone calls with faxed confirmations.

Secondly, we are still in the early innings of consolidation. Equity Lifestyle Properties owns or has controlling interest in more than 450 communities and resorts with over 170,000 sites. Sun Communities has approximately 179,700 developed sites across 671 properties. PE has also entered the game, with Northgate Holdings holdings having spent about $1 billion on resort construction and expansion. However, the market is still extremely fragmented. Out of the top 3 major players, ELS owns 4.2% of total revenue, Target Hospitality owns 3.7%, and Sun Communities owns 2.2%, making up less than 10% of total revenue in the industry.

Finally, the only clear winners established have been in the government sector (~47% of the market). ReserveAmerica was founded in 1984 and developed a reservation system for state and federal parks in 1992. Government contracts drove early innovation, with the ReserveAmerica to ACTIVE Network to Aspira spinoff creating a dominant player processing over 50 million bookings annually before being acquired by Alpine. Private campground software, meanwhile, has largely remained a cottage industry until recently.

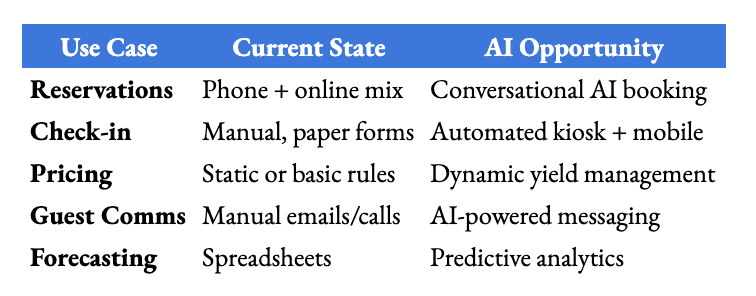

3. The Case for AI

Campground software faces the same administrative burden that plagued healthcare, legal, and other professional services, with almost the exact same pain points: manual reservation entry and confirmation, phone-based booking, paper check-in processes, and disconnected systems across PMS, POS, and utilities.

The market expansion case mirrors what we’ve seen in other verticals: AI reduces the cost to serve smaller operators, making the long tail of mom-and-pop ownership economically viable to address at scale.

4. Summary, Implications

Having spent time sourcing for search funds, this market fragmentation seems to mirror early dental and veterinary software; 78% independent ownership with aging operators looks like a classic PE rollup opportunity for both real estate and software. With Campspot giving the blueprint for platform expansion, going from PMS → Marketplace → Channel Management → Revenue Management, the vertical “super app” seems to be emerging. But with an industry this fractured, there is still runway left for other apps.

As OTA pressure drives software adoption, and Hipcamp and The Dyrt start taking share, parks will need direct booking tools, and the ROI on software becomes obvious when their 20% commission keeps eating away at low margins.

To us, the question isn’t whether software wins, it’s which model (transaction-based vs. flat-fee vs. marketplace vs. direct) captures the most value as consolidation accelerates.

Our takeaways for software Investors and Operators:

White space exists: Revenue management is the obvious expansion opportunity (either via acquisition by a PMS leader or standalone entry), and a category defining vertical camping app has yet to emerge.

Roll-up dynamics: The long tail of smaller players (40+ identified vendors) creates consolidation opportunities similar to what we’ve seen in adjacent verticals.

International arbitrage: European players (Camping.care, pod.camp) and Australian heritage companies (RMS Cloud, Newbook) present potential acquihire or geographic expansion targets.

Thanks for reading — feel free to reach out to thesoftwarepulse@gmail.com for any recommendations or inquiries. Until next time!